Thinking about an Adjustable-Rate Mortgage? Read This First.

Thinking about an Adjustable-Rate Mortgage? Read This First.

If you’ve been searching for a home recently, you’ve likely felt the impact of today’s mortgage rates. Combined with rising prices, it’s led many buyers to consider alternative financing options to help with affordability—like adjustable-rate mortgages (ARMs).

If the 2008 housing crash comes to mind, that’s understandable. But today’s ARMs are very different. Here’s how.

In the past, some borrowers were approved for ARMs they couldn’t afford once rates reset. Now, lending standards are much stricter. Lenders carefully assess whether borrowers can still manage payments even if the rate increases. So, the rise in ARM usage today isn’t a warning sign—it’s more about buyers finding flexible ways to make homeownership possible in a challenging market.

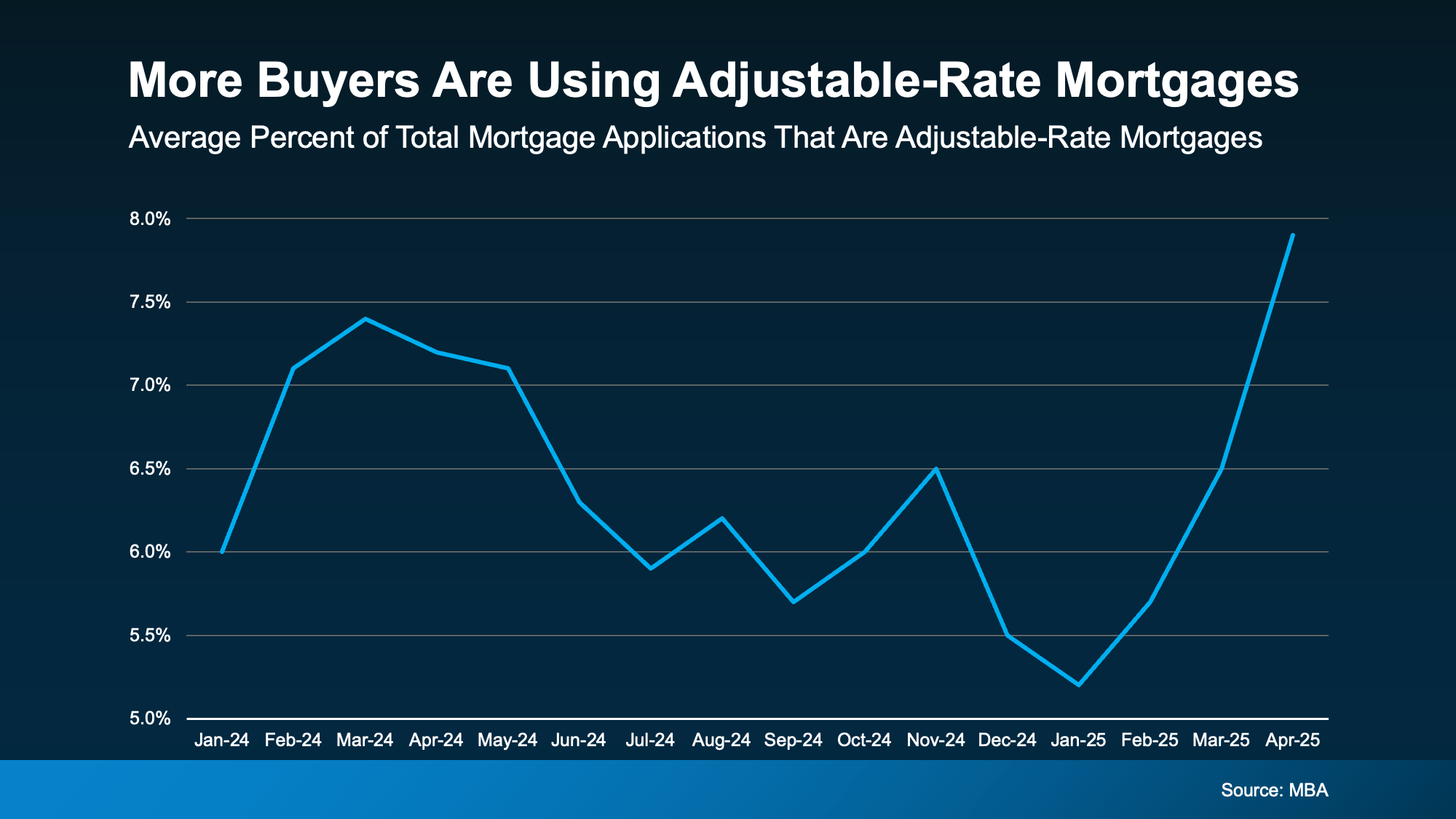

This shift is reflected in recent Mortgage Bankers Association (MBA) data, showing more buyers choosing ARMs right now (see graph below):

And while adjustable-rate mortgages (ARMs) aren’t the best fit for everyone, they can offer certain advantages depending on your situation.

How Adjustable-Rate Mortgages Work

Business Insider describes the key difference between fixed-rate and adjustable-rate loans this way:

“With a fixed-rate mortgage, your interest rate remains the same for the entire time you have the loan. This keeps your monthly payment the same for years . . . adjustable-rate mortgages work differently. You'll start off with the same rate for a few years, but after that, your rate can change periodically. This means that if average rates have gone up, your mortgage payment will increase. If they've gone down, your payment will decrease.”

With a fixed-rate mortgage, your base monthly payment remains steady, though costs like taxes and insurance may shift over time. ARMs, however, adjust after the initial fixed term.

Pros and Cons of Choosing an ARM

There are reasons why some buyers are considering ARMs again. One of the biggest draws is the typically lower starting interest rate. As Business Insider puts it:

"Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. With a lower ARM rate, you can get a smaller monthly payment or afford more house than you could with a fixed-rate loan."

But you also need to think about the potential for increased costs later. Barron’s highlights this reality:

"Adjustable-rate loans offer a lower initial rate, but recalculate after a period. That is a plus for borrowers if rates come down in the future, or if a borrower sells before the fixed period ends, but can lead to higher costs if they hold on to their home and rates go up."

That’s why it’s important to think about how long you plan to stay in your home. Even though forecasts predict rates may ease in the next couple of years, that isn’t guaranteed.

Before moving forward with an ARM, speak with your lender and a financial advisor to ensure it’s a smart fit for your situation and your risk tolerance.

Bottom Line

ARMs can offer real benefits for some buyers, especially with high rates. But since they’re not ideal for everyone, it’s important to fully understand how they work and consider both the advantages and the potential long-term risks. Talking to trusted professionals can help you decide if this type of loan works for your financial goals.

Categories

Recent Posts